The Tennessee Comptroller’s Office has released an investigation involving Douglas Molnar, who served as Austin Peay State University’s (APSU) Head Track and Field and Cross Country coach from September 2004 until June 2019.

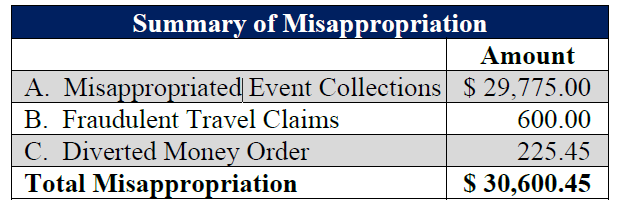

Investigators determined that Molnar misappropriated APSU funds totaling at least $30,600.45.

The vast majority of the misappropriated money was collected and turned over to Molnar during track and cross country fundraiser events hosted between 2015 and 2018. These fundraisers included several athletic events in which participants were charged entry fees. At least $29,775 that was collected during these events should have been deposited into an APSU bank account; however, investigators discovered that Molnar retained this money for his personal benefit.

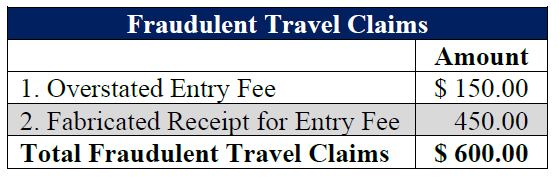

Molnar’s misappropriation also includes fraudulent travel claims totaling $600. Molnar either overstated or fabricated how much he had spent for the track team to attend track meets when he claimed reimbursement from the university.

Finally, Molnar diverted a money order totaling $225.45 into a bank account that he controlled. The money order was made payable to “Austin Peay” and should have been turned over to the university for deposit.

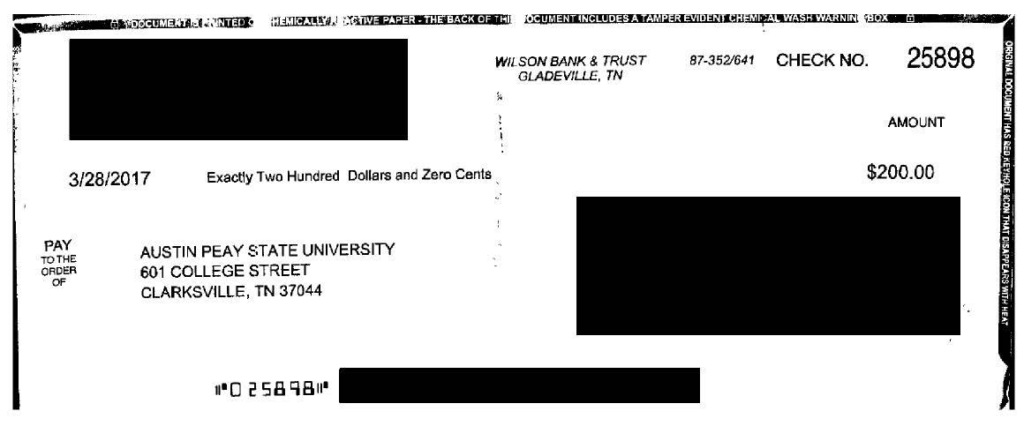

During the course of their investigation, investigators learned that Molnar deposited some of the misappropriated money into a joint checking bank account and a “Douglas Molnar, DBA Tennessee Athletic Project” bank account that he controlled. 21 of the checks he deposited into these accounts were made payable to APSU.

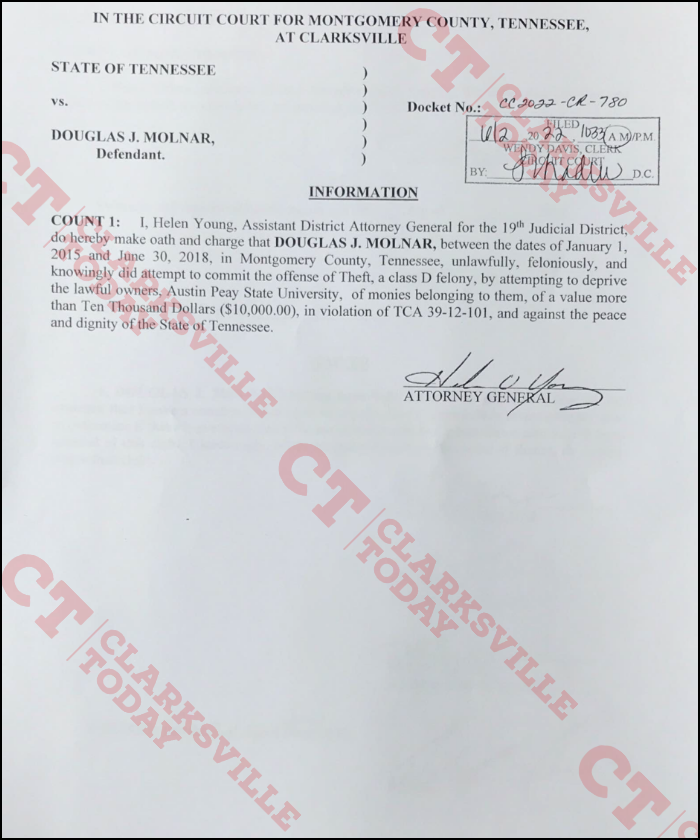

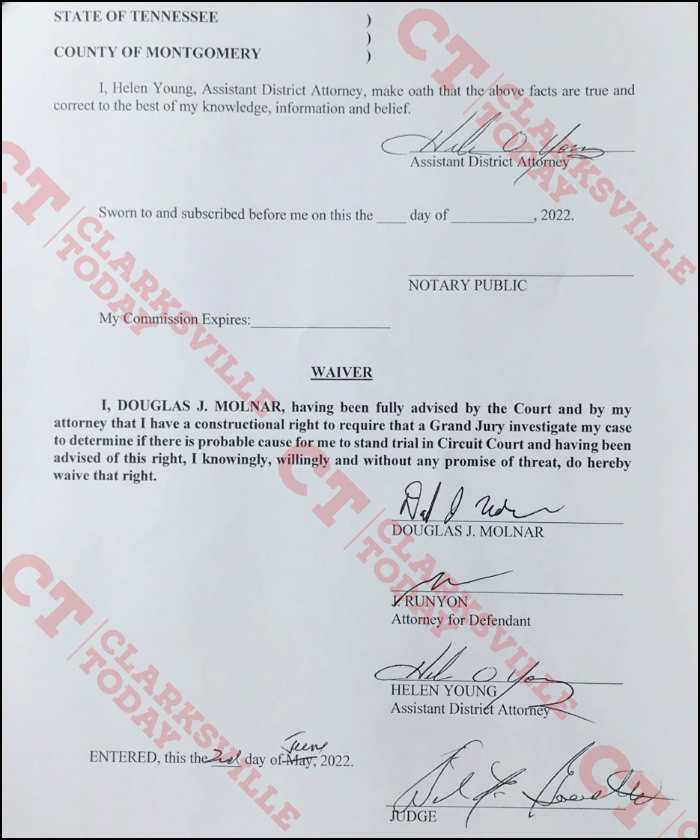

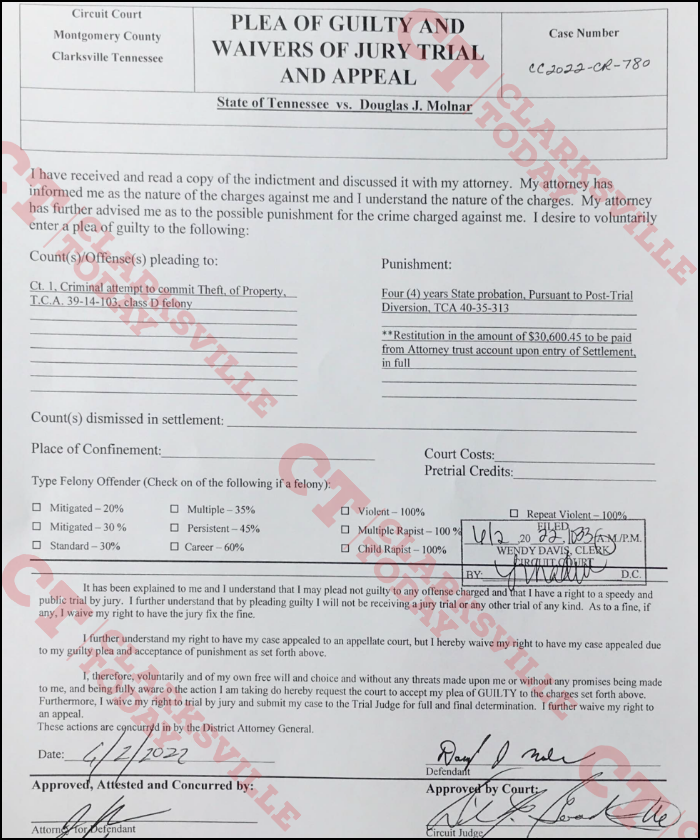

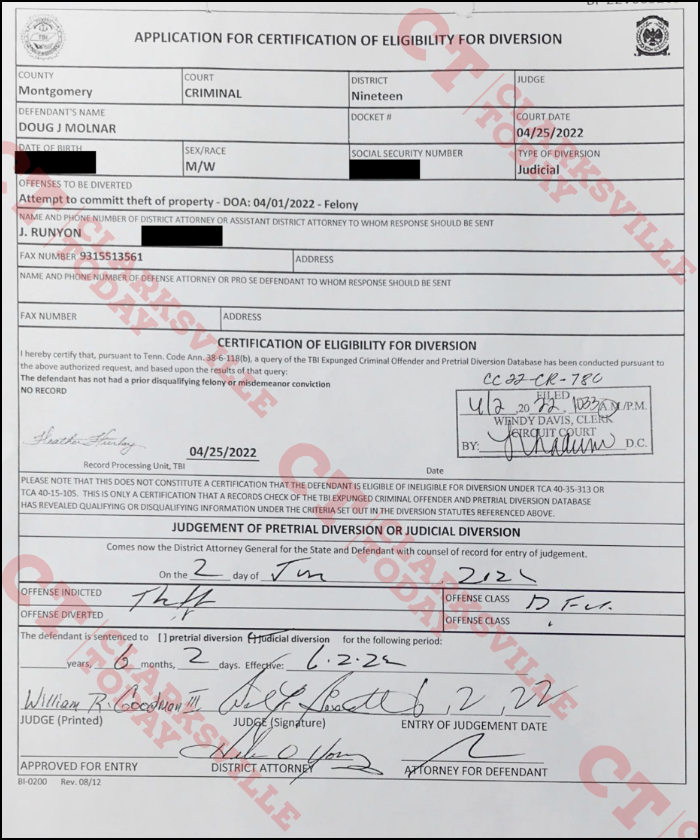

On June 2, 2022, Douglas Molnar entered a plea of guilty by criminal information in the Criminal Court of Montgomery County to the felony offense of theft of property over $10,000. The Court granted judicial diversion relief, placed Molnar on four years supervised state probation, and ordered him to pay restitution in the total amount of $30,600.45.

“We appreciate that Austin Peay officials reported these allegations to our Office,” said Comptroller Jason Mumpower. “As a result of these findings, we encourage the university to ensure that fundraiser collections from track and cross country events are turned over for deposit to university accounts. Collected amounts should also be reconciled with deposits to reduce the chance of misappropriation.”

During the period January 1, 2015, through June 30, 2018, former track and cross country

coach Douglas Molnar misappropriated APSU funds totaling $30,600.45. Molnar employed

the following three schemes to misappropriate funds for his personal benefit without the

authority or knowledge of APSU officials:

Misappropriated Fundraiser Event Collections totaling $29,775

Molnar misappropriated fundraiser event cash and check collections entrusted to him

totaling $29,775 from both track and cross country fundraiser events for his personal

benefit. Participants were charged entry fees to compete in the fundraiser events. Entry

fees were turned over to Molnar for deposit into the university’s bank account.

However, Molnar withheld collections from the 2016 and 2018 Austin Peay Governors

Invitational events ($10,365); the 2015, 2016, 2017, and 2018 High School Classic

events ($12,020); the 2015, 2016, and 2017 Wilma Rudolph Relay events ($2,200);

and the 2015, 2016, and 2017 Cross Country Festival events ($5,190) and retained the

entire amount of $29,775 for his personal benefit.

Registration information inappropriately instructed participants to make checks

payable to Tennessee Athletic Project (TAP) and mail the checks to Douglas Molnar

at APSU for the 2015, 2016, 2017, and 2018 High School Classic events. Investigators

determined that Molnar established, maintained, and controlled a bank account “Doing

Business As” (DBA) Tennessee Athletic Project where some checks were deposited,

which enabled him to control and convert the funds for his personal use and benefit.

All entry fee payments should have been made payable to APSU and deposited into a

designated APSU bank account.

B. Fraudulent Travel Claims totaling $600

Molnar submitted fabricated receipts, as part of his travel claims to the university, to

claim reimbursements for entry fees he purportedly paid totaling $600, to which he was

not entitled, for two separate track events that APSU attended.

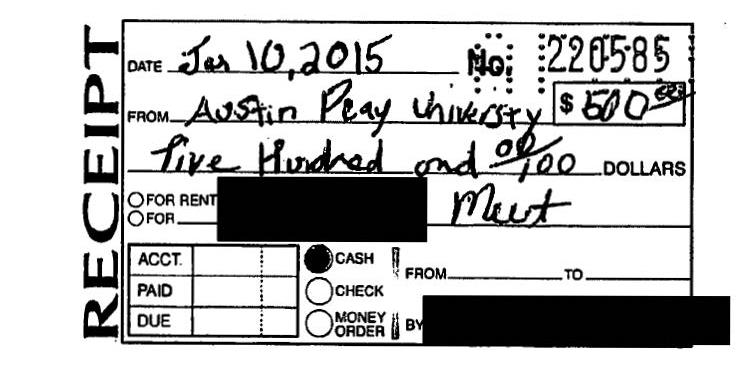

- On April 27, 2016, Molnar submitted a travel claim to APSU claiming he

paid the team’s $500 entry fee with his personal funds and was due reimbursement.

Although Molnar was due a reimbursement, he was only due reimbursement of

$350 – the actual amount of the entry fee he paid. Molnar effectively overstated

the amount of his entry fee payment and received an additional $150 ($500 less

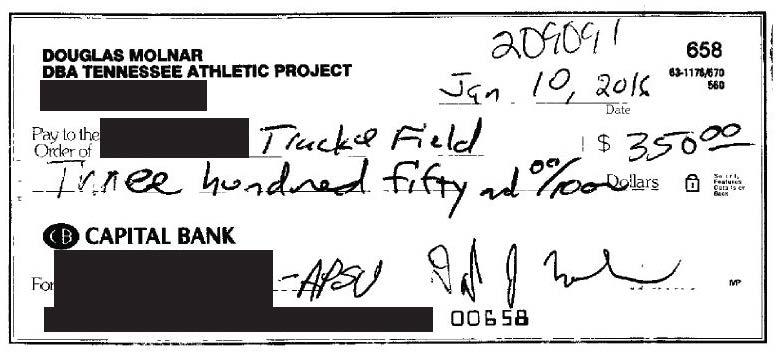

$350) from APSU to which he was not entitled. - To support his claim of the $500 entry fee, Molnar submitted to APSU the receipt he allegedly received from the host state university. However, the receipt that Molnar submitted as documentation appeared to have come from an APSU receipt book since it fell within the same receipt number sequence of other receipts APSU had issued to participants for APSU-hosted events. The event flier for the meet indicated APSU’s entry fee was $350. Additionally, Molnar issued a check from the DBA Tennessee Athletic Project bank account he controlled to cover the $350 entry fee.

travel claim in which he overstated an entry fee payment to

obtain $150, which he was not entitled.

due reimbursement of $350 from APSU. However, he fraudulently

submitted a receipt and claimed reimbursement for $500.

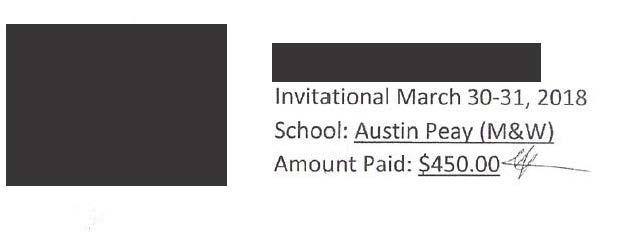

On March 30-31, 2018, APSU’s track team attended an invitational meet in

Missouri. On June 25, 2018, Molnar submitted a travel claim for reimbursement of

$450 for the entry fee that he supposedly paid with his personal funds. In fact, there

were no entry or other associated fees for the event. Molnar submitted to APSU a

fabricated receipt and effectively received $450 from APSU to which he was not

entitled.

payment to obtain a $450 reimbursement, which he was not entitled.

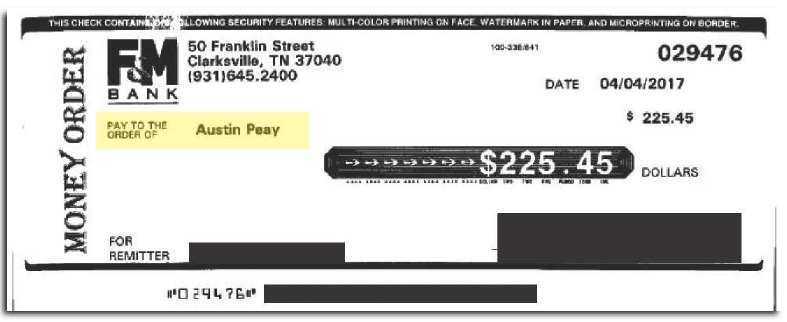

Diverted Money Order Collection totaling $225.45

Molnar diverted a money order totaling $225.45, intended for APSU, into a bank

account he controlled for his personal benefit. APSU had a contract with a vendor to

handle concessions at APSU athletic events, including some track fundraiser events.

The vendor sold concessions and gave a percentage of the proceeds to APSU. The

concessions vendor issued a money order payable to “Austin Peay” on April 4, 2017,

three days after the April 1, 2017, High School Classic track fundraiser event. [Refer

to Exhibit 4.] Instead of turning over the funds for deposit with APSU, on May 24,

2017, Molnar deposited the money order into a bank account he controlled for his

personal benefit.

APSU that Molnar diverted for his personal benefit.

FORMER TRACK AND CROSS COUNTRY COACH DOUGLAS MOLNAR DEPOSITED MISAPPROPRIATED FUNDS TOTALING $12,695.45 INTO BANK ACCOUNTS HE CONTROLLED

Molnar deposited $12,695.45 in misappropriated funds noted in Finding 1. above into bank

accounts he controlled for his personal benefit instead of depositing the funds into an APSU

bank account. Molnar deposited the misappropriated money order totaling $225.45 from the

concessions’ vendor as well as $12,470 in misappropriated event fundraiser check collections

into a joint checking bank account and a “Douglas Molnar, DBA Tennessee Athletic Project”

(TAP) bank account he controlled. Twenty-one of the checks he deposited into his bank

accounts were made payable to APSU. [Refer to Exhibit 5.] Investigators were unable to

determine whether any of the misappropriated entry fee cash collections were deposited into

his TAP or other personal bank accounts.

account that he controlled for his personal benefit.